Brazilian Law 15.042/2024: Regulatory Framework and Practical Guidelines for Companies with Carbon Inventory Obligations

Connecting Urgency and Regulation: From Diagnosis to Action

In a previous article, we discussed the “Brazilian Sustainability Market: Between Urgency and Inertia”, identifying the paradox of corporate sustainability in Brazil — companies waiting for external incentives while climate pressure intensifies. Today, we move from diagnostic analysis to a technical and practical approach: how Law 15.042/2024 transforms this landscape of anticipation into concrete obligations and structured opportunities.

The enactment of Law 15.042, on December 11, 2024, represents the materialization of previously discussed expectations. What was once a regulatory gap is now a structured framework, requiring Brazilian companies to adopt a proactive stance regarding their greenhouse gas emissions.

Brazilian Business Landscape: Assessing the Impact

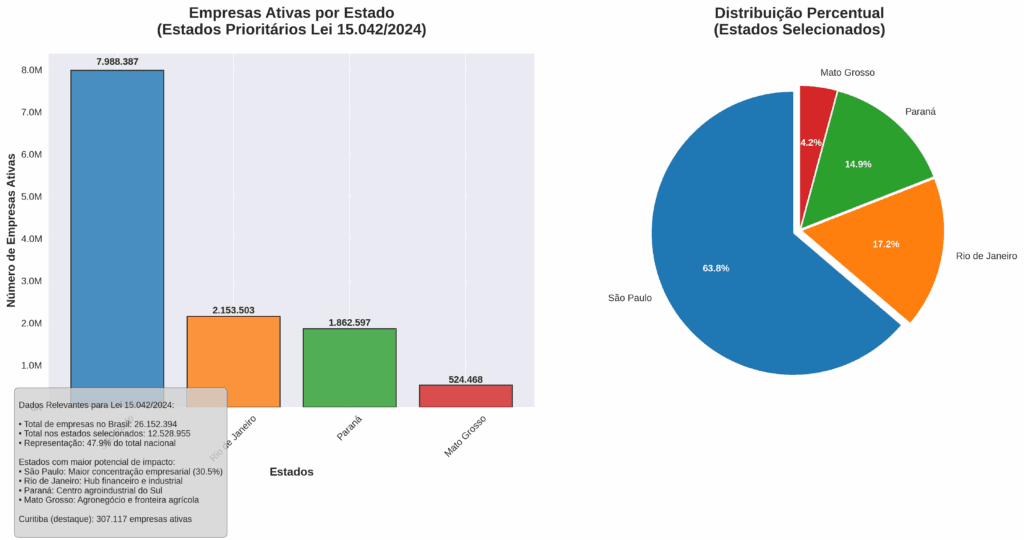

To understand the magnitude of the new legislation’s impact, it is essential to analyze the Brazilian business environment. According to official data from 2024, Brazil has over 26.1 million active companies, heterogeneously distributed across the country.

Regional Distribution of Active Companies

• São Paulo: 7,988,387 active companies (30.5% of the national total)

• Minas Gerais: 2,736,848 (10.5%)

• Rio de Janeiro: 2,153,503 (8.2%)

• Paraná: 1,862,597 (7.1%)

• Rio Grande do Sul: 1,657,264 (6.3%)

Regional Focus: Strategic States for Implementation

Mato Grosso: With 524,468 active companies and an economy heavily reliant on agribusiness, the state hosts high-emission activities and serves as a natural testing ground for the new carbon inventory rules.

Curitiba: The capital of Paraná, with 307,117 active companies, is recognized for its innovation in urban sustainability. The city already has consolidated environmental management initiatives, making it a model for implementing Law 15.042 obligations.

Brazilian Emissions Trading System (SBCE): Structure and Functioning

Law 15.042/2024 establishes the Brazilian Emissions Trading System (SBCE), a regulated carbon market based on the “cap and trade” model. It builds upon existing voluntary initiatives like B4 (the Climate Action Exchange) and Agente do Clima.

Tradable Assets under SBCE

- Brazilian Emissions Allowance (CBE) • Granted by the managing authority • Can be issued for free or at a cost • Grants the right to emit one ton of CO₂ equivalent

- Verified Emission Reduction or Removal Certificate (CRVE) • Based on verified mitigation project results • Can offset compliance (within set limits) • May be traded internationally with authorization

Implementation Phases

Phase 1 (2025–2027): Preparatory Period

• Management body setup

• Methodology development

• Operator training

Phase 2 (2028–2030): Pilot Implementation

• Initial compliance for specific sectors

• Free allocation of CBEs

• Monitoring and adjustments

Phase 3 (2031 onward): Full Operation

• Expansion to all regulated sectors

• Gradual introduction of CBE auctions

• International market integration

Carbon Inventory Obligations: A Practical Guide for Companies

Eligibility Criteria

Companies emitting more than 10,000 tons of CO₂ equivalent annually must submit yearly greenhouse gas inventories.

Priority Sectors

• Electricity generation

• Steel and metallurgy

• Cement and lime

• Pulp and paper

• Oil and natural gas

• Commercial aviation

Inventory Methodologies

• Scope 1: Direct emissions from sources controlled by the company

• Scope 2: Indirect emissions from purchased electricity, heat, or steam

• Scope 3: Other indirect emissions (when applicable), such as:

– Supply chain emissions

– Product use

– Transportation and distribution

Corporate Implementation Schedule

2025: Preparation and Training

• Mapping of emission sources

• Implementation of monitoring systems

• Training of technical teams

2026: First Pilot Inventory

• Data collection from 2025

• Third-party verification

• Submission to regulatory authority

2027: Adjustments and Improvements

• Refinement of methodologies

• Correction of non-conformities

• Preparation for mandatory phase

2028: Start of Formal Obligations

• Regulatory inventories required

• Potential penalties for non-compliance

• Participation in the CBE market

Strategic Opportunities and Competitive Advantages

Monetization of Energy Efficiency

Companies that have already invested in energy efficiency and emission reductions will be able to monetize those efforts through the sale of surplus CBEs or the generation of CRVEs.

Access to Green Financing

Compliance with Law 15.042 will facilitate access to:

• Sustainable credit lines

• Green bonds

• ESG investments

• Sustainable development funds

Market Differentiation

Companies that proactively implement carbon obligations will gain competitive advantage through:

• Improved corporate reputation

• Attraction of talent engaged with sustainability

• Preference among environmentally conscious consumers

• Increased valuation in capital markets

Implementation Challenges and Practical Solutions

| Challenge | Solution |

|---|---|

| Technical Capacity | Partnerships with universities and specialized consultancies for training |

| Monitoring Systems | Investment in IoT technologies and environmental management platforms |

| Implementation Costs | Use of specific financing lines and gradual rollout |

| Verification and Auditing | Development of a network of accredited verifiers and standardized processes |

Integration with Existing Initiatives

Convergence with the Voluntary Market

Law 15.042 does not replace the voluntary carbon market but creates a strategic convergence. Companies already participating in initiatives like B4 will have an advantage in transitioning to the regulated market, as they:

• Already have experience in carbon inventories

• Know the quantification and verification methodologies

• Have environmental management systems in place

• Understand how carbon markets work

Synergy with Agente do Clima

Tools like Agente do Clima, which already provide practical carbon management solutions, become even more relevant under a regulated framework, offering:

• Automated calculation platforms

• Traceability systems

• Interfaces with official registries

• Decision-making support

Strategic Recommendations by Company Size

Large Companies (>10,000 tCO₂e/year)

Immediate Actions:

- Establish a multidisciplinary carbon committee

- Map all emission sources

- Implement continuous monitoring systems

- Develop a compliance and optimization strategy

Priority Investments:

• Integrated environmental management systems

• Emission reduction technologies

• Internal staff training

• Strategic partnerships with verifiers

Medium Companies (5,000–10,000 tCO₂e/year)

Preventive Preparation:

- Monitor emissions to assess proximity to regulatory thresholds

- Implement energy efficiency measures

- Basic training in carbon management

- Evaluate potential for generating CRVEs

Small Companies (<5,000 tCO₂e/year)

Voluntary Opportunities:

- Join sectoral efficiency programs

- Take advantage of renewable energy incentives

- Develop CRVE projects

- Prepare for potential future inclusion in the system

Future Outlook and System Evolution

Sectoral Expansion

Law 15.042 provides for the gradual expansion of the SBCE to other economic sectors, including:

• Road and maritime transportation

• Agriculture and livestock

• Civil construction

• Large-scale retail and service sectors

International Integration

The Brazilian system is being designed to be compatible with:

• The European Union Emissions Trading System (EU ETS)

• The California and Quebec carbon markets

• Mechanisms under the Paris Agreement (Article 6)

• International verification standards

Technological Innovation

Emerging technologies expected to influence the SBCE include:

• Blockchain for asset traceability

• Artificial Intelligence for emissions optimization

• Remote sensing for monitoring

• Digital trading platforms for accessibility and scale

Conclusion: From Inertia to Climate Leadership

Law 15.042/2024 represents Brazil’s definitive shift from a scenario of “urgency and inertia” to a structured framework for climate action. For Brazilian companies—especially those located in states with the highest business concentrations such as São Paulo, Rio de Janeiro, Paraná, and Mato Grosso—this moment is a unique opportunity to transform regulatory obligations into competitive advantages.

Success in implementing Law 15.042 will depend on companies’ ability to see beyond compliance, recognizing carbon inventory obligations as a strategic tool for:

• Operational optimization

• Energy cost reduction

• Access to new markets

• Strengthening corporate branding

• Preparation for a low-carbon future

Companies that begin their preparation journey today, leveraging the experience already accumulated by initiatives like B4 and Agente do Clima, will be better positioned to lead Brazil’s energy transition and seize the opportunities of a growing and robust carbon market.

Regulation has arrived. The question is no longer “if” companies will need to adapt, but “how quickly” they can turn adaptation into competitive differentiation.

Brazil’s sustainable future depends on this collective response from the business sector.

This article is based on Law 15.042/2024 and official data on the Brazilian business landscape. For specific implementation guidance, consultation with carbon management specialists and continued monitoring of complementary regulations published by the SBCE’s managing body is recommended.

🌍 About B4 — The First Climate Action Exchange

Official Website: https://b4.capital/en

Instagram: https://www.instagram.com/b4.capital/

LinkedIn: https://www.linkedin.com/company/empresa-b4-capital/

E-mail: contato@b4.capital

🤖 About Agente do Clima

Agente do Clima is B4’s artificial intelligence that performs carbon footprint assessments based on the GHG Protocol, delivering results in under 24 hours.

🌐 Access now: https://agentedoclima.com

0 comentários